The United Arab Emirates (UAE) has recently introduced a Corporate Tax Law that is set to take effect from the beginning of the financial year starting on or after June 01, 2023. This law will apply to all companies and branches that are operating within the country, including foreign entities, highlighting the Impact of UAE CT on Foreign Companies and their tax obligations.

The impact of the corporate tax on foreign companies will depend on a number of factors, which will be discussed in detail in subsequent sections.

For the purpose of this law, foreign companies are referred to non-resident entities that are not incorporated under any state or federal law within the UAE.

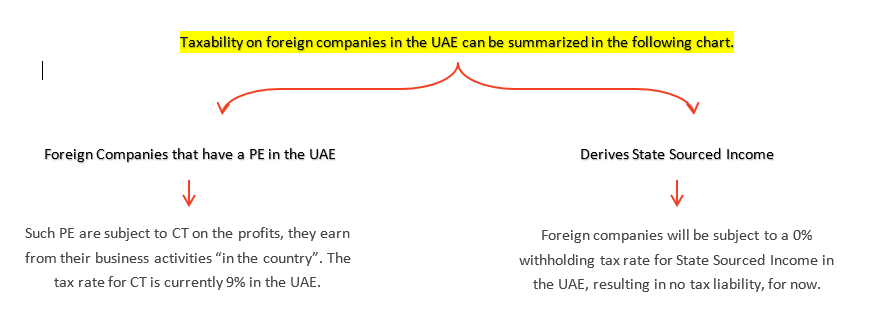

Under the newly implemented Corporate Tax Law in the UAE, non-resident persons may be subject to taxation in two scenarios.

Firstly, if the non-resident person is conducting business operations in the UAE through a Permanent Establishment (PE), then they will be subject to Corporate Tax (CT) on the profits earned from their business activities in the country. The current CT rate in the UAE is 9%.

Non-residents are subject to corporate tax on their total profits earned in a relevant financial year, without any threshold limit. This means that non-residents will not be able to claim the exemption of up to AED 375,000, which is available to resident companies.

Note: For further understanding of what constitutes a PE, please refer to our article on “Permanent Establishment”.

Secondly, if a foreign company derives State Sourced Income from their business activities in the UAE, they will be subject to withholding tax as per Article 45 of Federal Decree Law No. 47. It is important to note that the current rate of withholding tax is 0%, meaning there will be no tax liability on such arrangements for now. However, it is crucial to be aware that the rate of withholding tax may be revised in the future based on any subsequent decision issued by the Cabinet at the suggestion of the Minister.

Foreign companies with a PE in the UAE will need to keep in mind the tax implications of their business activities and take appropriate measures to ensure compliance with the Corporate Tax Law. Furthermore, companies deriving State Sourced Income should stay informed of any updates or changes to the withholding tax rate.

It is true that foreign companies are liable to UAE CT on total profits, still there are some exemptions and incentives to available for foreign entities / Non-residents. For example, Income derived by a Non-Resident Person from operating aircraft or ships in international transportation that meets the conditions of Article 25 of this Decree-Law.

In conclusion, as the coin has two sides, the UAE corporate tax also has both positive and negative impacts on foreign companies doing business in the country.

Whereas the tax increases the cost of doing business in the UAE for foreign companies, the introduction of corporate tax has also helped to create a more stable and predictable business environment in the UAE, increasing foreign companies’ confidence in investing in the country in the long term.

The UAE government’s commitment of generating revenue through taxation has sent a clear message to foreign investors that the country is serious about building a sustainable economy.

Also read : Impact of CT to Freezone Companies