The introduction of Corporate Tax in the UAE marked a significant shift in the country’s business landscape. As businesses adapt to the new tax framework, compliance with registration and filing requirements has become more important than ever. One of the most common issues faced by businesses is failing to register for Corporate Tax within the timeframe prescribed by the Federal Tax Authority (FTA). Missing registration deadlines can lead to administrative penalties, unnecessary compliance risks, and increased scrutiny from tax authorities.

Whether you operate a mainland company, a Free Zone business, a branch of a foreign company, or a sole establishment, understanding your Corporate Tax obligations is essential to avoid costly mistakes. In this blog, we explain the Corporate Tax registration requirements, common reasons businesses incur penalties, practical strategies to remain compliant, and how professional support can help safeguard your business.

Why Corporate Tax Registration Should Not Be Delayed

Many business owners view tax registration as an administrative formality. It is one of the most important compliance obligations under the UAE Corporate Tax regime. Registration establishes your business within the Federal Tax Authority’s tax system and enables the authority to monitor compliance with filing and reporting requirements. Delaying registration can create complications that extend beyond financial penalties. Businesses may face increased scrutiny, difficulties in maintaining compliance records, and challenges when preparing future tax returns.

Consider a newly established consultancy firm in Dubai. The management team may be focused on client acquisition, recruitment, and business development. Tax compliance often becomes a secondary priority. However, overlooking registration requirements can result in unnecessary penalties that could have been avoided through timely action. The cost of non-compliance is often far greater than the effort required to complete registration correctly from the outset.

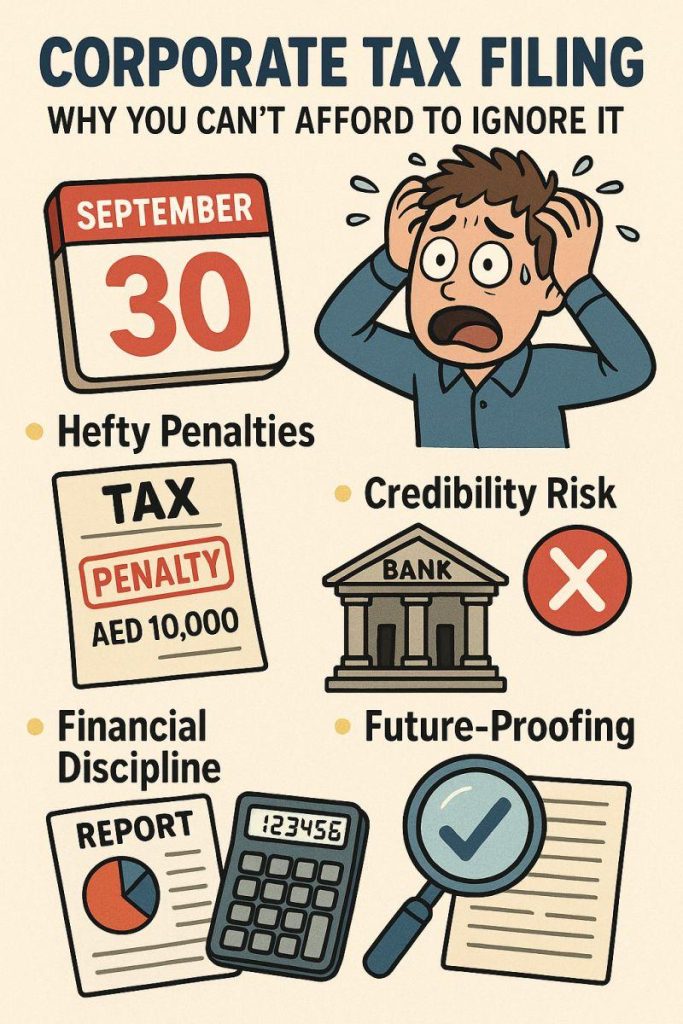

Corporate Tax Registration Penalties in UAE

Businesses that fail to register within the required period may face administrative penalties imposed by the FTA. Potential Consequences Include:

- Monetary penalties

- Additional compliance reviews

- Delayed processing of tax obligations

- Increased risk of future non-compliance issues

Since FTA regulations can be updated periodically, businesses should regularly review official guidance and seek professional assistance where necessary.

Common Reasons Businesses Receive FTA Penalties

1. Missing Registration Deadlines

Many companies assume Corporate Tax registration can be postponed until filing season. This is one of the most common compliance mistakes.

2. Incorrect Company Information

Errors in:

- Trade License Details

- Business Activities

- Contact Information

- Ownership Structure

may delay registration approval.

3. Failure to Monitor FTA Announcements

The FTA periodically issues updates, guides, and registration requirements. Businesses that fail to monitor these changes may unintentionally become non-compliant.

4. Poor Record Keeping

Insufficient documentation often creates compliance challenges during tax assessments and audits.

Corporate Tax Registration Penalty (Most Common FTA Fine)

If a business fails to register for Corporate Tax within the prescribed deadline, the Federal Tax Authority may impose an administrative penalty of AED 10,000. This is a fixed penalty and applies even if the business has not generated taxable income.

Other Common Corporate Tax Penalties

| Violation | Approximate Penalty |

|---|---|

| Late Corporate Tax Registration | AED 10,000 |

| Late Corporate Tax Return Filing | AED 500 per month for the first 12 months, increasing thereafter |

| Failure to Maintain Required Records | AED 10,000 per violation |

| Repeated Record-Keeping Violations | AED 20,000 |

| Failure to Submit Tax Documents in Arabic (when requested) | AED 5,000 |

| Late Corporate Tax Deregistration Application | AED 1,000 per month (up to AED 10,000) |

| Late Payment of Corporate Tax | Additional penalties and interest may apply on outstanding tax amounts |

How to Avoid Corporate Tax Registration Penalties

Register Early

- Do not wait until the deadline approaches.

- Early registration allows sufficient time to correct errors and complete verification requirements.

Maintain Accurate Business Records

Keep updated:

- Trade Licenses

- Financial Statements

- Ownership Records

- Contact Information

Monitor FTA Updates

Regularly review Federal Tax Authority announcements and guidance documents.

Conduct Periodic Compliance Reviews

A proactive review can identify issues before they result in penalties.

Work with Corporate Tax Experts

Professional advisors can help:

- Assess registration obligations

- Complete registration correctly

- Monitor compliance deadlines

- Prepare documentation

Corporate Tax Compliance Checklist

- Verify Corporate Tax applicability

- Confirm registration deadline

- Prepare supporting documents

- Register through FTA portal

- Obtain Tax Registration Number (TRN)

- Maintain accounting records

- Track filing obligations

- Conduct annual compliance review

Conclusion

Corporate Tax compliance is no longer optional for UAE businesses. Timely registration, accurate documentation, and proactive compliance management are essential to avoiding penalties and maintaining regulatory confidence. By understanding your obligations and implementing strong compliance processes, businesses can minimize risk, avoid costly fines, and focus on sustainable growth. If you are unsure about your Corporate Tax registration obligations, consulting experienced tax professionals can help ensure full compliance while protecting your business from unnecessary penalties.